Europe gas prices set to fall amid high storage levels throughout 2024

Gas prices in Europe could fall as low as US$6.70 per MMbtu in the summer as the mild winter will see storage levels remain above 55% according to a new report by Wood Mackenzie.

The report, ‘‘Europe gas and power markets short-term outlook Q1 2024’, states that the mild European winter, the second in succession, means that European storage levels will reach 89% by the end of July 2024, putting further pressure on prices.

“With storage levels nearing full capacity towards the end of the summer, there will be up to 10 bcm of excess supply that will need to either be piped into underground storage facilities in Ukraine or floated in LNG vessels”. says Mauro Chavez, Director of Europe Gas & LNG Markets at Wood Mackenzie. “This means that a higher summer-winter differential is required to balance the market, compared to what the current forward curve suggests, putting downward pressure on Q3 prices.

European demand rebound under normal weather and improved economic performance

The report states that gas demand remained suppressed in 2023, falling 16% versus the five-year average, amid mild weather and lower demand from power generation. However, 2024 started off strong as colder weather swept through Europe supporting distribution demand. Industrial demand maintained its recovering trend, increasing 12% year-on-year in January and around 6% in February.

The report forecasts that household gas demand in Europe looks set to rise by 12 billion cubic metres (bcm) in 2024, under normal weather conditions, while industrial demand will increase by 5.5 bcm as the EU economy rebounds in the second half of the year. However, the report adds that 9 bcm less gas will go into power generation reducing the impact of residential and industrial demand growth. Overall European demand is set to increase 9 bcm.

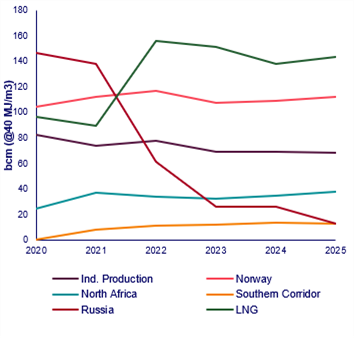

European gas flows

Source: Wood Mackenzie

Russian flows via Ukraine will be key to market dynamics in 2025

European prices are set to increase in 2025. Despite much new LNG supply being commissioned in 2024 and 2025, LNG year-on year supply growth will be limited to 15 MMtpy in 2025, as projects will take time to ramp up while some legacy LNG supply will continue to decline. As a result, we anticipate that LNG imports to Europe will only increase by 4.5 MMtpy in 2025.

The report concludes that Russian gas flows through Ukraine will be the key dynamic to watch in 2025. If the end of the transit agreement between Russia and Ukraine results in a complete stop of flows, then Europe could see storage levels limited to 93% by the of summer 2025, providing upside to prices. However, if an agreement is found to transit flows through Ukraine, then European prices would come under more pressure.

Related News

Related News

- ADNOC deploys pioneering AI-enabled process optimization technology

- Mexico Pacific announces long-term LNG SPA with POSCO International

- ONEOK to acquire Medallion and controlling interest in EnLink for $5.9 B

- Golar LNG signs EPC deal for $2.2-B MK II FLNG conversion project

- Japan's Mitsubishi to acquire stake in Petronas LNG plant

Comments