U.S. LNG developers sign highest volume of sale and purchase contracts since 2022

U.S. LNG sale and purchase agreements from perspective projects.

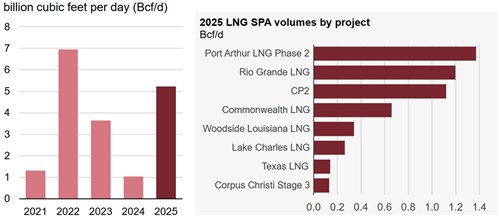

U.S. developers signed sale and purchase agreements (SPA) for 40 million tons per annum of liquefied natural gas (LNG) in 2025 from planned export facilities, according to U.S. Department of Energy (DOE) and company website data. This LNG volume equals 5.2 billion cubic feet per day (Bcf/d), the highest volume since 7.0 Bcf/d in 2022.

SPAs specify the terms and conditions of transactions between sellers and buyers, including LNG volumes, contract length, pricing, and liquefaction fees. SPAs are essential to securing a final investment decision (FID) for LNG terminal construction. In addition to SPA agreements, financial institutions usually require a complete set of approvals from both DOE and the Federal Energy Regulatory Commission to reach FID. Favorable contract terms and increased demand for LNG in Europe and Asia contributed to the rise of SPA signings in 2025. In addition, DOE resumed LNG export permit reviews following a pause initiated in 2024, which had slowed developers’ ability to secure SPAs.

Developers of Port Arthur Phase 2 contracted 1.4 Bcf/d of export capacity in 2025, the most nationwide, followed by Rio Grande Phase 2 with 1.2 Bcf/d, CP2 with 1.1 Bcf/d, and Commonwealth LNG with 0.7 Bcf/d. Developers of four other terminals signed the remaining 0.9 Bcf/d. Over 90% of LNG volumes sold in 2025 were under free-on-board SPAs, compared with 100% of volumes in 2024. Under free-on-board SPAs, international buyers take ownership of and pay for the purchased LNG exports at the producing country’s loading terminal.

Approximately 95% of volumes sold were under 20-year SPAs, effective when commissioning is complete and the projects begin long-term commercial operations. For pricing, 56% of sold volumes are confirmed to be indexed to the U.S. benchmark Henry Hub natural gas price, compared with 67% in 2024. LNG contract pricing is usually linked to Henry Hub or to Brent crude oil futures and is often a percentage of the contract price.

Most LNG volumes contracted in 2025 were split between offtake companies based in Europe and Asia, such as utilities, national oil and gas companies, and portfolio players. Offtakers in the Middle East contracted for a smaller share of volumes. However, SPA contracts commonly have destination flexibility, where buyers can deliver LNG to any destination as long as it complies with DOE export authorizations and U.S. law.

Developers reached FID on four LNG projects in 2025, bringing a combined 7.2 Bcf/d in nominal LNG export capacity under construction, according to the EIA's Liquefaction Capacity File. The planned in-service date of these projects ranges from 2029–31:

- Woodside Louisiana LNG Phase 1 (2029)

- CP2 Phase 1 (2029)

- Rio Grande Phase 2 (2030–31)

- Port Arthur Phase 2 (2031)

In December 2025, Energy Transfer announced it would suspend its development of Lake Charles LNG but is exploring a sale to a third-party developer.

Related News

Related News

- RWE strengthens partnerships with ADNOC and Masdar to enhance energy security in Germany and Europe

- TotalEnergies and Mozambique announce the full restart of the $20-B Mozambique LNG project

- Venture Global wins LNG arbitration case brought by Spain's Repsol

- KBR awarded FEED for Coastal Bend LNG project

- Norway pipeline gas export down 2.3% in 2025, seen steady this year

Comments